|

Thursday, November 15, 2018

FOR IMMEDIATE RELEASE Contact: Caroline Peattie, Fair Housing Advocates of Northern California (415) 483-7552, peattie@fairhousingnorcal.org Fair Housing Advocates of Northern California and Client Settle National Origin Discrimination Complaint San Rafael, CA – Late last month, Fair Housing Advocates of Northern California (FHANC) and one of its clients settled a complaint alleging discrimination based upon national origin that had been filed with the Department of Fair Employment and Housing against Continuum Housing Association – San Rafael Redevelopment Agency and its agents. Adan Bernardino Peralta was a prospective tenant who applied for and was subsequently denied the opportunity to rent a two-bedroom apartment at Lone Palm Court Apartments, 840 C Street in San Rafael, California in August 2017. Mr. Peralta’s household was to include his wife and their two minor children (aged 17 and 10 at the time). Mr. Peralta is a naturalized U.S. citizen born in Mexico. His wife, born in Colombia, was a resident in the United States with a valid tourist visa.

0 Comments

Civil Rights Organizations Accuse Bank of America of Housing Discrimination in 37 Metropolitan Areas6/26/2018 For Immediate Release June 26, 2018 Contact: Contact: Caroline Peattie, Fair Housing Advocates of Northern California peattie@fairhousingnorcal.org - (415) 483-7552 Civil Rights Organizations Accuse Bank of America of Housing Discrimination in 37 Metropolitan Areas Fair Housing Advocates of Northern California, National Fair Housing Alliance, 18 other Fair Housing Organizations, and Two Homeowners Allege Bank of America and Safeguard Properties Management Violated the Federal Fair Housing Act Today, Fair Housing Advocates of Northern California (FHANC), the National Fair Housing Alliance (NFHA), 18 other fair housing organizations, and two homeowners in Maryland filed a federal Fair Housing Act lawsuit against Bank of America, N.A., Bank of America Corp., and Safeguard Properties Management, LLC (“Bank of America/Safeguard”). The lawsuit alleges Defendants intentionally failed to provide routine exterior maintenance and marketing at Bank of America-owned homes in working- and middle-class African-American and Latino neighborhoods in 37 metropolitan areas, while they consistently maintained similar bank-owned homes in comparable white neighborhoods. Below is an example of a Bank of America property in a neighborhood of color in Vallejo, which demonstrates a number of issues that invite further problems.  The boarded door and window reduce marketability, are unappealing, and make the home dark inside. These boards are also not protecting the windows from breaking since the boards are on the inside of the house.  Bank of America failed to clean up the yard and secure holes, allowing rodents and cats into the home’s crawlspace. Click here to download the complete press release. Download the complete complaint below.

Thursday, April 19, 2018

FOR IMMEDIATE RELEASE Contact: Caroline Peattie, Executive Director, Fair Housing Advocates of Northern California (415) 483-7552 / peattie@fairhousingnorcal.org Looking Back 50 Years to Chart the Future: Fair Housing Advocates of Northern California convenes forum highlighting 50th anniversary of Fair Housing Act's passage to inform how past accomplishments can help with future challenges Last week marked the 50th anniversary of the passage of the Fair Housing Act of 1968. This piece of legislation had been filibustered in the Senate by segregationists until the Kerner Commission released its reports that civil unrest was due to the existence of "two societies, one black, one white - separate and unequal." This galvanized the Senate to pass the bill, but the House did not follow suit until after the assassination of Dr. Martin Luther King Jr. and seven days of civil unrest followed. Walter Mondale's New York Times Op-Ed piece was published on the day of the anniversary of the Fair Housing Act and clearly charts the political events that led to the passage of the Act, as well as the intent of the Act. "The act has survived long enough to witness a curious debate over its intent," he writes. "Some scholars have suggested that its functions can be divided into "anti-discrimination" and "integration," with the two goals working at cross purposes. At times, critics suggest the law's integration aims should be sidelined in favor of colorblind enforcement measures that stamp out racial discrimination but do not serve the larger purpose of defeating systemic segregation. To the law's drafters, these ideas were not in conflict. The law was informed by the history of segregation, in which individual discrimination was a manifestation of a wider societal rift." The main purpose of the Act, the co-author of the civil rights bill maintains, was to create integrated communities, and intended to accomplish this in private markets by making housing discrimination illegal in the sale, rental, or advertising of housing, and through the federal bureaucracy, by requiring government agencies to administer their programs in a manner that "affirmatively furthers fair housing." Although many today are surprised to learn this fact, one of the strongest proponents of the Act and of integration was Republican George Romney, Secretary of Housing and Urban Development, who had the following response to one township's contention that progress was being made and forced integration was unnecessary and even resented: "The youth of this nation, the minorities of this nation, the discriminated of this nation are not going to wait for 'nature to take its course.' What is really at issue here is responsibility - moral responsibility." (Charles M. Lamb,Housing Segregation in Suburban America Since 1960, pp. 85-93.) It was not until 2015 that HUD promulgated its Affirmatively Furthering Fair Housing rule laying out very clear guidelines on how federal agencies would be expected to ensure that federal funds would be used to further fair housing. Nevertheless, the concept of furthering fair housing and integrating communities was inherent in the Fair Housing Act, a mandate that grew out of an understanding that this country must counter decades of institutionalized racism and discrimination that led to the segregation we see today, locally and nationally. Richard Rothstein's book, The Color of Law - A Forgotten History of How Our Government Segregated America, acknowledges the collective amnesia that has allowed for continued neighborhood segregation in municipalities and has led to social strife across the country. View Richard Rothstein's talk at a local 2016 conference on this topic, here. Fair Housing Advocates of Northern California celebrates the 50th anniversary of the passage of the Fair Housing Act next Wednesday, April 25, looking at the history of the Act, its successes and shortcomings, and how best to chart a path forward. The event will bring together fair housing and tenant advocates, lenders, real estate agents and developers, housing providers, city and county staff, elected officials, and community members. The conference commemorating the historic event will feature speakers and panelists from Marin, the Bay Area, California, and the east coast to make it a profound event, particularly against the backdrop of the state of civil rights in our country today and the current administration. The two plenary sessions in the morning (titled "California: The Frontline in the War to Integrate America's Cities"and "The Fair Housing Act at 50 - Where do we go from here?" respectively) will lay the foundation for the panels in the afternoon: For Tenants: Tenant Rights and Protections - This session will unpack housing-related bills recently passed as well as what is on the horizon, and how they apply locally; and how various organizing groups can work together to effect change. For Housing Developers, Realtors, Lenders: Sustainable Homeownership Among Low-to-Moderate Income and Minority Borrowers - This session will focus on policies that foster inclusive communities and best practices for transparency and responsible borrowing and lending. Gentrification and Displacement - This panel will address issues of racial equity and land preservation, how policies and institutions limit mobility and equity-building, and other issues. Affirmatively Furthering Fair Housing - Looking at our local history and how policies affecting access to transportation, education, and affordable housing shaped the segregated living patterns we see today, panelists will suggest tools to further fair housing, particularly related to supporting affordable housing, public schools, and transportation policies that will begin to reverse patterns of segregation and lack of access. Strengthening housing advocacy through alliance building - This panel will address how to have difficult conversations about housing in our neighborhoods by debunking myths, stereotypes and misinformation that often lead to fear and exclusion. People interested in more information and registration can visit http://bit.ly/FHANCConference2018. Fair Housing Advocates of Northern California is a non-profit organization serving several Bay Area counties that provides free counseling, enforcement, mediation, and legal or administrative referrals to persons experiencing housing discrimination. Fair Housing Advocates of Northern California also offers foreclosure prevention services, pre-purchase education, seminars to help housing providers fully understand fair housing law, and education programs for tenants and the community at large. Fair Housing Advocates of Northern California is a HUD-Certified Housing Counseling Agency. The mission of Fair Housing Advocates of Northern California is to ensure equal housing opportunity and to educate the community on the value of diversity in our neighborhoods. Please call Fair Housing Advocates of Northern California at (415) 457-5025 or TDD: (800) 735-2922 for more information. April 6, 2018

FOR IMMEDIATE RELEASE Contacts: Adriana Ames / adriana@fairhousingnorcal.org Caroline Peattie / peattie@fairhousingnorcal.org RE: Upcoming Fair Housing Conference, April 25, 2018 Fair Housing Advocates of Northern California is pleased to present the upcoming 2018 Conference: “Past Accomplishments, Future Challenges - Celebrating 50 Years of the Fair Housing Act” to be held on Wednesday, April 25, 2018, 8:30 a.m. - 5:30 p.m. at the Embassy Suites Hotel, 101 McInnis Parkway in San Rafael. The Fair Housing Conference will commemorate the 50th Anniversary of the passage of the Fair Housing Act, featuring experts in the fair housing field who will address pressing fair housing concerns affecting Marin and the Bay Area, and offer opportunities to engage in strategies to further fair housingin local communities, given present and future challenges at the local, state, and national levels.The conference will gather community members, advocates, real estate professionals, municipal leaders, service providers, and the business community. The featured speakers are James Perry, CEO of the Winston-Salem Urban League, and George Lipsitz, Professor of Black Studies and Sociology, University of California, Santa Barbara. The program includes concurrent panels on tenant rights and protections, sustainable homeownership, gentrification and displacement, and on affirmatively furthering fair housing. The closing panel will focus on strengthening housing advocacy through alliance building. Pre-registration is required to attend. The registration fee is $45 per person and includes a catered lunch. Partial scholarships are available upon request; visit our conference page for more information. To register, visit our conference page at http://www.fairhousingnorcal.org/fair-housing-conference-2018.html For more information or for any special needs, please contact Adriana Ames, Education Director, at adriana@fairhousingnorcal.org. The conference is funded in part bya grant from the U.S. Department of Housing and Urban Development, and the California State Bar, and co-sponsored by: Marin Community Foundation, Wells Fargo Bank, Mechanics Bank, Luther Burbank, First Federal Savings, PRANDI Property Management, TIAA/EverBank, Marin Sanitary Services, Consumer Action and Marin Economic Forum. ------------------------------------------------------------------------------------------------------------------------- Founded as a non-profit in 1986, Fair Housing Advocates of Northern California, FHANC serves several Bay Area counties, providing counseling, investigation, mediation and legal referrals to persons experiencing housing discrimination. FHANC conducts outreach activities and offers programs that educate the community about fair housing and the value of diversity, and also conducts preventive trainings for housing providers, and provides pre-purchase education and foreclosure prevention counseling. FHANC is a HUD-Certified Housing Counseling Agency. Please contact FHANC at (415) 457-5025 or TDD: (800) 735-2922 for more information or visit www.fairhousingnorcal.org. Wednesday, February 14, 2018

FOR IMMEDIATE RELEASE Contact: Caroline Peattie, Executive Director, Fair Housing Advocates of Northern California (415) 483-7552 / peattie@fairhousingnorcal.org or Casey Epp, Supervising Attorney, Fair Housing Advocates of Northern California casey@fairhousingnorcal.org Fair Housing Advocates of Northern California and Plaintiffs Settle Housing Complaint Alleging National Origin, Familial Status, and Disability Discrimination San Rafael, CA – Last week, Fair Housing Advocates of Northern California (FHANC, formerly Fair Housing of Marin) and two of its clients signed a settlement related to a complaint of discrimination in housing based upon national origin, familial status, and disability, filed with the Department of Housing and Urban Development (HUD) and later transferred to California’s Department of Fair Employment and Housing (DFEH). The complaint was filed against Rosa Nguyen and Bob Torreso, the owner and the property manager, respectively, of 150 Clark Street, San Rafael, where the plaintiffs resided with their minor son. Bob Torreso was the primary agent in contact with the clients regarding their tenancy. The clients were represented by Marcus Levy, FHANC’s Bilingual Housing Counselor, and Casey Epp, FHANC’s Supervising Attorney, who also represented the agency. The case was successfully mediated by DFEH for a total of $27,200 in damages and included fair housing training for three years as well as significant policy changes. FOR IMMEDIATE RELEASE February 1, 2018 Contact: Contact: Caroline Peattie, Fair Housing Advocates of Northern California peattie@fairhousingnorcal.org - (415) 483-7552 Deutsche Bank, Ocwen Financial, and Altisource Accused of Racial Discrimination in 30 U.S. Metro Areas National Fair Housing Alliance, Fair Housing Advocates of California, and 18 Civil Rights Groups File Federal Lawsuit Over Neglected Foreclosures in Communities of Color PowerPoint available here. Download a PDF version of the press release here. Read the filed complaint here. Today, Fair Housing Advocates of Northern California (FHANC) joined the National Fair Housing Alliance (NFHA) and 18 fair housing organizations from across the country filed a housing discrimination lawsuit in federal district court in Chicago, IL against Deutsche Bank; Deutsche Bank National Trust; Deutsche Bank Trust Company Americas; Ocwen Financial Corp.; and Altisource Portfolio Solutions, Inc. Ocwen and Altisource are the servicer and property management company responsible for maintaining and marketing a large number of Deutsche Bank’s properties. NFHA is filing this lawsuit on the first day of Black History Month to highlight how neglected bank-owned homes hurt African American communities. The lawsuit alleges that Deutsche Bank purposely failed to maintain its foreclosed bank-owned homes (also known as real estate owned or “REO” properties) in middle- and working- class African American and Latino neighborhoods in 30 metropolitan areas, while it consistently maintained similar bank-owned homes in white neighborhoods. The data presented in the federal lawsuit, which is supported by substantial photographic evidence, shows a stark pattern of discriminatory conduct by Deutsche Bank/Ocwen/Altisource in the maintenance of foreclosed homes. The poor maintenance of homes in communities of color resulted in these homes having wildly overgrown grass and weeds, unlocked doors and windows, broken doors and windows, dead animals decaying, and trash and debris left in yards. Deutsche Bank/Ocwen/Altisource are paid and under contract to provide routine maintenance and marketing to these bank-owned homes. This includes regular lawn mowing, securing a home’s windows and doors, covering dryer vent holes and other holes to keep animals and insects from nesting, keeping the property free of debris, trash, branches and weeds, and complying with nuisance abatement ordinances in each city. The lawsuit is the result of a multi-year investigation undertaken by NFHA and its fair housing agency partners beginning in 2010. “We chose to first file administrative complaints with HUD against Deutsche Bank, expecting the bank to review our evidence and implement changes to secure, maintain, and market its bank-owned homes in communities of color to the same standard it did in white neighborhoods,” said Shanna L. Smith, President & CEO of NFHA. “However, even after meeting with Deutsche Bank’s legal counsel in April 2015 and sharing photographs illustrating the significant differences in treatment between homes in African American/Latino and white neighborhoods, we saw no improvement,” Smith continued. NFHA also met with representatives from Ocwen and Altisource and shared photographs illlustrating these problems. No improvements with routine maintenance and marketing issues were identified following those meetings, so NFHA and the 19 fair housing agencies amended the HUD complaint to add these companies. The lawsuit points out that Deutsche Bank-owned homes in predominantly white working- and middle-class neighborhoods are far more likely to have the lawns mowed and edged regularly, invasive weeds and vines removed, windows and doors secured or repaired, litter, debris and trash removed, leaves raked, and graffiti erased from the property. Below are photos of Deutsche Bank’s foreclosed homes from largely non-white neighborhoods that illustrate the result of the neglect of the properties. Deutsche Bank-owned home in a non-white community in Richmond (left) and Antioch (right). Boarded homes, holes in eaves, and bent gutters were just some of the deficits found at this Fairfield home. In contrast, the pictures below show well-kept neighbors’ homes in non-white neighborhoods which are negatively impacted by the foreclosed properties next door. Neighbors’ homes, well maintained, in non-white communities. In predominantly white neighborhoods, on the other hand, Deutsche Bank’s foreclosed properties were better maintained and marketed, as seen in the photos below. Deutsche Bank-owned home in a white community in Benicia (left) and Brentwood (right). “We initially investigated Deutsche Bank’s properties in 2014 in Solano and Contra Costa counties and found really badly maintained properties in communities of color,” said Caroline Peattie, Executive Director of Fair Housing Advocates of Northern California. “Despite Deutsche Bank being on notice about the problems with their foreclosed properties, they still had not been addressed when we investigated properties in 2016 and found similar issues. Again and again, in neighborhoods that were predominantly Latino or non-white, we found Deutsche Bank properties covered in dead grass, missing professional ‘for sale’ signs marketing the home, littered with garbage, and marred by broken or boarded windows, damaged fences, and the like. Even a highly scored property in a majority non-white neighborhood in Vallejo, built in 2004 and in good shape, was completely unsecured, inviting vandals to waltz through the door. That is unconscionable.” NFHA and the 19 partner agencies collected evidence at each property on over 35 data points that were identified as important to protecting and securing the homes. Investigators also took and closely reviewed nearly 30,000 photographs of Deutsche Bank-owned homes to document the differences in treatment between communities of color and white neighborhoods. NFHA conducted repeat visits to several Deutsche Bank-owned homes over the course of the investigation. However, investigators found little or no improvement in maintenance and often found the homes in worse condition. FHANC investigated a total of 22 Deutsche Bank properties in the Vallejo and Richmond metro areas, 5 of which were located in predominantly Latino communities, 13 REOs in a community with a majority of non-White residents and 4 in predominantly White communities. Photos of the properties in the counties of Solano and Contra Costa can be viewed on FHANC’s PowerPoint at here.

The poor appearance of Deutsche bank-owned homes in middle- and working-class neighborhoods of color destroys the homes’ curb appeal for prospective homebuyers and invites vandalism because the homes appear to be abandoned. Additionally, the blight created by Deutsche Bank/Ocwen/Altisource results in a decline in home values for African American and Latino families who live next door or nearby, deepening the racial wealth gap and inequality in America. This is not a new problem for Deutsche Bank. In June 2013, Deutsche Bank, as trustee and owner of record of foreclosed homes, settled a lawsuit with the City of Los Angeles for $10 million after it was accused of allowing hundreds of foreclosed properties to fall into slum conditions, leading to the destabilization of whole communities. In the past, Deutsche Bank has taken the position that as a trustee of the loans that resulted in foreclosure, it has no legal obligation to maintain the properties once they come into Deutsche Bank’s possession. And yet, Deutsche Bank agreed to settle the City’s claims and required its preservation maintenance companies to pay most of the $10 million to resolve that case. Under the Fair Housing Act, trustees are clearly liable for discriminatory activity to the same extent as any other owner of property. NFHA alleges that Deutsche Bank, Ocwen, and Altisource’s intentional failure to correct their discriminatory treatment in African American and Latino neighborhoods—the same communities hardest hit by the foreclosure crisis—can only be seen as systemic racism. Smith stated, “The intentional neglect of bank-owned homes in communities of color devalues the property and the lives of the families living in the neighborhoods around them. The health and safety hazards created by these blighted Deutsche Bank-owned homes affect the residents, especially the children, living nearby.” Smith continued, “It is important to note that Deutsche Bank, Ocwen, and Altisource were all paid to secure, maintain, and market these homes. No one is asking for special treatment of these bank-owned homes; we simply ask that these companies provide the same standard of care for all bank-owned homes, regardless of the racial or ethnic composition of the neighborhood in which they are located.” Stagnant water and overgrown grass, commonly documented at homes where Deutsche Bank is owner of record in African American and Latino neighborhoods through this investigation, are a fertile habitat for mosquitos, rodents, termites, roaches, and other pests. “We found unsecured pools with stagnant water in non-white communities, which is not only a breeding ground for mosquitoes, but also very dangerous for adventurous and curious children,” said Peattie. Pool is unsecured and has stagnant water in a non-white community in Antioch, CA. Pool is maintained and secured by a locked gate in a white community in Brentwood, CA.

In addition, pests often carry diseases such Zika and Hantavirus and present serious health risks to nearby residents. These vermin infestations commonly spread to nearby homes. “To compound these problems,” Peattie adds, “overgrown dead grass and shrubbery pose a fire hazard for homes in California – and we’ve seen the terrible destruction of major fires in the past few months. Bank-owned properties must be properly maintained.” In 2011, NFHA released the first of three reports documenting poor routine maintenance of foreclosed homes in African American and Latino neighborhoods as compared to foreclosures in white neighborhoods. Many photographs of poorly-maintained bank-owned homes were shared. Each report recommended best practices to avoid Fair Housing Act violations. “We truly hoped the release of the reports, which included advice on how to comply with civil rights laws, would change the banks’ behavior,” said Smith. “However, only a few banks reached out for meetings to develop best practices, and Deutsche Bank was not one of them.” The second report was released in 2012 and the last one in 2014. The HUD complaint was filed and then amended to add additional cities and new evidence on the following dates: February 26, 2014; April 30, 2014; August 7, 2014; January 22, 2015; August 5, 2016; February 14, 2017; and July 26, 2017. NFHA and its member agencies are represented by Soule, Bradtke & Lambert and Relman, Dane & Colfax PLLC. What does intentional discrimination look like? http://nationalfairhousing.org/Deutsche-Photos http://nationalfairhousing.org/community-map The Fair Housing Act makes it illegal to discriminate based on race, color, national origin, religion, sex, disability, or familial status, as well as on the race or national origin of residents of a neighborhood. This law applies to housing and housing-related activities, which include the maintenance, appraisal, listing, marketing, and selling of homes. Fair Housing Advocates of Northern California is a non-profit organization serving several Bay Area counties that provides free counseling, enforcement, mediation, and legal or administrative referrals to persons experiencing housing discrimination. Fair Housing Advocates of Northern California also offers foreclosure prevention counseling and pre-purchase education, seminars to help housing providers fully understand fair housing law, and education programs for tenants and the community at large. Fair Housing Advocates of Northern California is a HUD-Certified Housing Counseling Agency. The mission of Fair Housing Advocates of Northern California is to ensure equal housing opportunity and to educate the community on the value of diversity in our neighborhoods. National Fair Housing Alliance Founded in 1988, the National Fair Housing Alliance is a consortium of more than 220 private, non-profit fair housing organizations, state and local civil rights agencies, and individuals from throughout the United States. Headquartered in Washington, D.C., the National Fair Housing Alliance, through comprehensive education, advocacy, enforcement programs, and neighborhood-based community development programs provides equal access to apartments, houses, mortgage loans, and insurance policies for all residents in the nation. The work that provided the basis for this publication was supported, in part, by funding under a grant with the U.S. Department of Housing and Urban Development. The author and publisher are solely responsible for the accuracy of the statements and interpretations contained in this publication. Such interpretations do not necessarily reflect the views of the Federal Government. ### Contact:

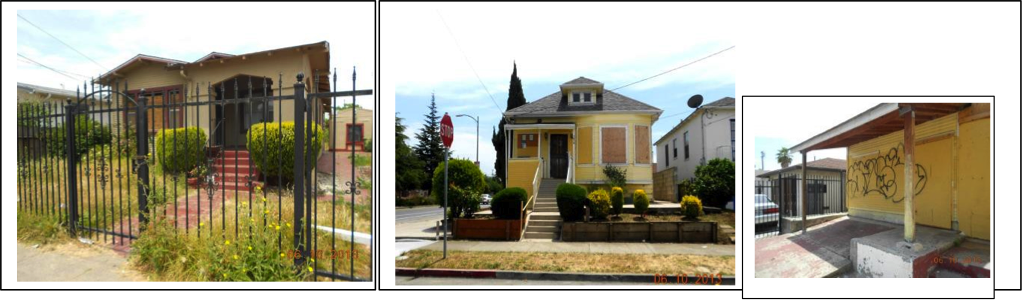

Caroline Peattie, Executive Director, Fair Housing Advocates of Northern California (415) 483-7552 / peattie@fairhousingnorcal.org or Casey Epp, Supervising Attorney, Fair Housing Advocates of Northern California casey@fairhousingnorcal.org Fair Housing Advocates of Northern California and a Plaintiff Settle Disability Complaint Last month, Fair Housing Advocates of Northern California (FHANC, formerly Fair Housing of Marin) and one of its clients signed a settlement related to a complaint of discrimination in housing based upon disability, filed with the Department of Housing and Urban Development’s Fair Housing office. The complaint was filed against Schultz Investment Co., Greenbrae Management Incl, Belardo Co., L.P., and Thomas Allhoff, Vice President of Schultz. Allhoff was the primary agent in contact with the client regarding her assistance animal at the Bon Air Apartments in Greenbrae. The complaints were filed in late 2016 and early 2017. Stacy Kitchin brought the action against her landlord, alleging violations of the federal Fair Housing Act and related state laws on the basis of race and disability, and was joined in the complaint by FHANC, which alleged disability discrimination. Ms. Kitchin was represented by Casey Epp, Supervising Attorney for FHANC. The case was conciliated by HUD for a total of $72,000 in damages and included fair housing training as well as significant policy changes. Stacy Kitchin, a disabled African-American woman, moved in with her small service dog at Bon Air Apartments in Greenbrae over 15 years ago. She initially requested and was approved for a reasonable accommodation in 2010 to have her service animal with her. However, despite having permission to have her service animal with her, Mr. Allhoff sent Ms. Kitchin repeated notices alleging lease violations because of her service animal. In addition, he accused her small dog of attacking maintenance workers. She provided proof to the contrary, both through letters of support through neighbors, as well as evidence that her dog was not present during one alleged attack. “I want everyone to know that people with disabilities deserve the same opportunities to enjoy their living space as others, and that landlords need to consider reasonable accommodation requests,” said Ms. Kitchin. “It was difficult to get over the disrespect I experienced with Mr. Allhoff. Andrea Schultz hired Mr. Allhoff, who put me down and abused me with his words and threats to my tenancy for years. I am thankful for the help I received from Fair Housing Advocates of Northern California with my complaint. They spent a lot of time and I appreciated their expertise. Thanks to them, Andrea Schultz will know the importance of hiring people who follow the law and I hope she and Mr. Allhoff learn something from the fair housing training they are required to take.” In May 2014, Ms. Kitchin contacted Fair Housing Advocates of Northern California for assistance after receiving a 3-Day Notice to Cure or Quit, requiring the removal of her service animal. FHANC’s staff attorney contacted Allhoff, informing him of the law and requesting a rescission of the notice. Ultimately, he complied and granted the request; however, he continued to implement discriminatory policies regarding assistance animals. FHANC received several calls for assistance from people with disabilities in 2014 and 2015, and intervened a number of times, reiterating to Mr. Allhoff the protections afforded to disabled individuals who require assistance animals, including companion animals, in their home. FHANC conducted its own investigation, conducting two paired site tests and a single, stand-alone site test for disability discrimination at the Greenbrae leasing office. “Despite numerous interventions from our office, a housing provider managing hundreds of units knowingly violated fair housing laws for years,” said Casey Epp. “I worry about all of the potential tenants and prospective tenants who experienced discrimination and did not contact our office for assistance. It’s important for landlords to know that there are consequences for disregarding fair housing laws and the impact discrimination can have on tenants.” In addition to the payment of damages to both complainants, the housing providers have agreed to the following: creating and implementing a written reasonable accommodation and reasonable modification policy advising employees, tenants and prospective tenants that an emotional support or companion animal may qualify as a reasonable accommodation under the Fair Housing Act; changing the lease to remove discriminatory language and notify existing tenants of the revised lease; implementing a tracking system for reasonable accommodation and modification requests, (providing this tracking sheet to HUD with dates of request, approval/denial, and other information on an annual basis for three years); attending a live fair housing training on an annual basis for two years; displaying HUD’s assistance animal poster in its leasing office and garbage facilities, and other relief. “On an ongoing basis, our agency receives many calls from people with disabilities who need reasonable accommodations,” said Caroline Peattie, FHANC’s Executive Director. “Many of those calls concern service and companion animals; both must receive the same consideration under fair housing law. When a person with a disability requests an accommodation, the housing providers may require documentation that there is a disability and that the request will address that need, but they are required to consider each request individually and engage in an interactive dialogue with the tenant.” Fair Housing Advocates of Northern California is a non-profit organization serving several Bay Area counties that provides free counseling, enforcement, mediation, and legal or administrative referrals to persons experiencing housing discrimination. Fair Housing Advocates of Northern California also offers foreclosure prevention services, pre-purchase education, seminars to help housing providers fully understand fair housing law, and education programs for tenants and the community at large. Fair Housing Advocates of Northern California is a HUD-Certified Housing Counseling Agency. The mission of Fair Housing Advocates of Northern California is to ensure equal housing opportunity and to educate the community on the value of diversity in our neighborhoods. Please call Fair Housing Advocates of Northern California at (415) 457-5025 or TDD: (800) 735-2922 for more information. National Fair Housing Alliance, Fair Housing Advocates of Northern California, and 18 other Fair Housing Center Partners Charge Deutsche Bank and its Preservation Maintenance Companies with Housing Discrimination based on Race and National Origin PowerPoint available here. A PDF version of the press release is here. View the amended complaint here. Today, Fair Housing Advocates of Northern California (FHANC) joined the National Fair Housing Alliance (NFHA) and other partners in announcing its collection of new evidence in support of allegations that Deutsche Bank, Ocwen Financial, and Altisource companies continue to discriminate against communities of color in 30 metropolitan areas across the United States. The 20 agencies allege that Deutsche Bank AG, Deutsche Bank National Trust, Deutsche Bank Trust Company Americas, Ocwen Financial Corporation, and Altisource Portfolio Solution, Inc. fail to provide required routine maintenance on bank-owned homes in middle- and working-class African American and Latino neighborhoods, while Deustche/Ocwen/Altisource consistently provide routine maintenance on similar bank-owned homes in white neighborhoods. Poorly maintained bank-owned properties create a harmful and dangerous environment for the local community. They also drive down the property value of homes owned by neighbors – causing the overall community to be economically depressed. The practice of neglecting foreclosed properties in African American and Latino communities increases the economic divide, perpetuates segregation, and denies people within these communities the right to fair and safe housing. The slipshod boarding of a window in an Antioch home; piles of trash at a Richmond home; and boarded window, holes in eaves and bent gutters of a Fairfield home, all in largely non-white neighborhoods, illustrate Deutsche Bank's neglect. In contrast, the pictures below show well-kept neighbors’ homes in non-white neighborhoods which are negatively impacted by the foreclosed properties next door. In predominantly white neighborhoods, on the other hand, Deutsche Bank’s foreclosed properties were better maintained and marketed, as seen in the photos below of homes in Benicia (left) and Brentwood (right). The administrative complaint filed with the Department of Housing and Urban Development (HUD) adds Ocwen and Altisource as respondents because Deutsche Bank uses these companies to provide preservation maintenance and marketing for the overwhelming majority of properties where the Bank is listed as owner of record. FHANC, NFHA, and 18 other fair housing organizations joined together in filing this administrative complaint. The data presented in this complaint includes approximately 30,000 photographs of Deutsch Bank-owned homes in 30 metropolitan areas from communities of color and predominately white neighborhoods from coast-to-coast. The analysis of substantial photographic evidence shows a stark pattern of discriminatory conduct in the maintenance of bank-owned homes in communities of color. “We began investigating Deutsche Bank’s properties in 2014 in Solano and Contra Costa counties and found horribly maintained properties in communities of color,” said Caroline Peattie, Executive Director of Fair Housing Advocates of Northern California. “Despite Deutsche Bank being on notice about the problems with their foreclosed properties, they still had not been addressed when we investigated properties in 2016 and found similar issues. Again and again, in neighborhoods that were predominantly Latino or non-white, we found Deutsche Bank properties covered in dead grass, missing professional ‘for sale’ signs marketing the home, littered with garbage, and marred by broken or boarded windows, damaged fences, and the like. Even a highly scored property in a majority non-white neighborhood in Vallejo, built in 2004 and in good shape, was completely unsecured, inviting vandals to waltz through the door. That is unconscionable.” FHANC investigated a total of 22 Deutsche Bank properties in the Vallejo and Richmond metro areas, 5 of which were located in predominantly Latino communities, 13 REOs in a community with a majority of non-White residents and 4 in predominantly White communities. Photos of the properties in the counties of Solano and Contra Costa can be viewed on FHANC’s PowerPoint here.

NFHA asserts that Deutsche Bank’s properties in predominantly white working- and middle-class neighborhoods are far more likely to have the lawns mowed and edged regularly, invasive weeds and vines removed, windows and doors secured or repaired, litter and trash removed, leaves raked, and graffiti erased from the property. “Yet, Deutsche foreclosed homes in predominantly middle-and working-class African American and Latino neighborhoods are more likely to be left neglected with debris and trash on the property, wildly overgrown grass, and invasive plants covering the yards. Windows and doors are often unsecured, left wide open, or boarded, and graffiti as well as dead animals are left on the premises,” said Shanna Smith, President and CEO of NFHA. She added, “Poor maintenance destroys a home’s curb appeal and invites vandalism or squatters because the home appears to be abandoned.” Also, the blight caused by this neglect results in declining home values for African American and Latino families who live nearby, deepening the racial wealth gap and inequality in America. Additionally, poorly maintained bank-owned properties impact the health of the local community. According to a report by Mariana Arcaya, Sc.D., M.C.P for the American Heart Association, living near a foreclosed home can increase a person’s blood pressure “due in part to unhealthy stress from residents’ perception that their own properties are less valuable, their streets less attractive or safe and their neighborhoods less stable.” Windows, doors and holes left open, unsecured, or broken at vacant properties allow for water to accumulate and stagnate. As a result, Deutsche Bank’s poorly maintained homes serve as the perfect environment for mold and discoloration to develop. In fact, a recent study conducted by Midwest Aerobiology Labs found 36 molds specific to foreclosed homes and also concluded that 88 percent of foreclosed homes contained a dangerous mold capable of causing childhood asthma and other diseases in humans. Stagnant water and overgrown grass, commonly documented at homes where Deutsche Bank is owner of record in African American and Latino neighborhoods through this investigation, are also a fertile habitat for mosquitos, rodents, termites, roaches, and other pests. “We found unsecured pools with stagnant water in non-white communities, which is not only a breeding ground for mosquitoes, but also very dangerous for adventurous and curious children,” said Peattie. Below is an example of an unsecured pool with stagnant water in a non-white community in Antioch, CA (left) and a well-maintained pool maintained and secured by a locked gate in a white community in Brentwood, CA (right) In addition, pests often carry diseases such Zika and Hantavirus and present serious health risks to nearby residents. These vermin infestations commonly spread to nearby homes. “To add to these hazards,” Peattie adds, “overgrown dead grass and shrubbery pose a fire hazard for homes in California.”

"Just imagine the health impact the families in communities of color experience living next door or nearby those poorly maintained Deutsche Bank homes," said Smith. “By neglecting their properties, Deutsche Bank, Ocwen and Altisource are putting the health of African American and Latino residents living near these properties at risk.” “This isn’t a new problem for Deutsche Bank. In June 2013, Deutsche Bank settled a lawsuit with the City of Los Angeles for $10 million after they were accused of allowing hundreds of bank-owned properties to fall into slum conditions, leading to the destabilization of communities,” said Smith. “It’s my understanding that Deutsche Bank required its preservation maintenance companies to pay most of the $10 million to resolve that case, so you would expect Deutsche/Ocwen/Altisource to monitor maintenance to ensure these shameful, discriminatory practices of neglecting routine maintenance in middle/working class communities of color ended. Unfortunately, we still find these horrid conditions at too many bank-owned in communities of color,” said Smith. View map of affected communities: http://nationalfairhousing.org/community-map/ and view photos of the properties at http://nationalfairhousing.org/deutsche-property-photos/. Below is a list of the 30 metro areas involved in the investigation: Baltimore, MD Baton Rouge, LA Chicago, IL Cleveland, OH Columbus, OH Dallas, TX Dayton, OH Denver, CO Detroit, MI (suburban communities) Gary, IN Grand Rapids, MI Greater Palm Beaches, FL Hampton Roads, VA Hartford, CT Indianapolis, IN Kansas City, MO Memphis, TN Miami, FL Milwaukee, WI Minneapolis, MN Muskegon, MI New Orleans, LA Orlando, FL Philadelphia, PA Prince George’s County, MD/Washington, DC Providence, RI Richmond, VA Tampa, FL Toledo, OH Richmond/Vallejo, CA The fair housing organizations joining NFHA in filing the complaint include: Fair Housing Advocates of Northern California 1314 Lincoln Avenue, Suite A San Rafael, CA 94901 HOPE Fair Housing Center 202 W. Willow Ave, Suite 203 Wheaton IL 60185 Open Communities 614 Lincoln Avenue Winnetka, IL 60093 South Suburban Housing Center 18220 Harwood Avenue Homewood, IL 60430 Housing Opportunities Made Equal of Virginia 626 East Broad Street #400 Richmond, VA 23219 Toledo Fair Housing Center 432 North Superior Street Toledo, OH 43604 Fair Housing Continuum 4760 N US Highway 1, Suite 203 Melbourne, FL 32935 Greater New Orleans Fair Housing Action Center 404 S Jefferson Davis Pkwy New Orleans, LA 70119 Denver Metro Fair Housing Center 3280 Downing Street, Suite B Denver CO 80205 Metropolitan Milwaukee Fair Housing Council 759 N Milwaukee Street, Suite 500 Milwaukee, WI 53202 Fair Housing Center of West Michigan 20 Hall Street SE Grand Rapids, MI 49507 The Miami Valley Fair Housing Center 505 Riverside Drive Dayton, OH 45405 Housing and Research & Advocacy Center 2728 Euclid Avenue, Suite 200 Cleveland, OH 44115 Fair Housing Center of the Greater Palm Beaches 1300 W Lantana Road, Suite 200 Lantana, FL 33462 Fair Housing Center of Central Indiana 445 N. Pennsylvania Street, Suite 811 Indianapolis, IN 46204 Central Ohio Fair Housing Association 175 South 3rd Street, Suite 580 Columbus, OH 43215 Housing Opportunities Project for Excellence, Inc. 11501 NW 2nd Avenue Miami, FL 33168 Connecticut Fair Housing Center 221 Main Street, 4th Floor Hartford, CT 06106 North Texas Fair Housing Center 8625 King George Drive, Suite 130 Dallas TX 75235 NFHA and its member agencies are represented by Relman, Dane & Colfax PLLC and Soule, Bradtke & Lambert. Detailed statistics and photos are available at www.nationalfairhousing.org. The Fair Housing Act makes it illegal to discriminate based on race, color, national origin, religion, sex, disability, or familial status, as well as the race or national origin of residents of a neighborhood. This law applies to housing and housing-related activities, which include the maintenance, appraisal, listing, marketing, and selling of homes. Fair Housing Advocates of Northern California is a non-profit organization serving several Bay Area counties that provides free counseling, enforcement, mediation, and legal or administrative referrals to persons experiencing housing discrimination. Fair Housing Advocates of Northern California also offers foreclosure prevention services advice, seminars to help housing providers fully understand fair housing law and education programs for tenants and the community at large. Fair Housing Advocates of Northern California is a HUD-Certified Housing Counseling Agency. The mission of Fair Housing Advocates of Northern California is to ensure equal housing opportunity and to educate the community on the value of diversity in our neighborhoods. The National Fair Housing Alliance Founded in 1988, the National Fair Housing Alliance is a consortium of more than 220 private, nonprofit fair housing organizations, state and local civil rights agencies, and individuals from throughout the United States. Headquartered in Washington, D.C., the National Fair Housing Alliance, through comprehensive education, advocacy, and enforcement programs, provides equal access to apartments, houses, mortgage loans, and insurance policies for all residents in the nation. The work that provided the basis for this investigation was supported in part by funding under a grant from the U.S. Department of Housing and Urban Development. The substance and findings of the work are dedicated to the public. The author and publisher are solely responsible for the accuracy of the statements and interpretations contained in this release. Such interpretations do not necessarily reflect the views of the Federal Government. ### PowerPoint video presentation available here. A PDF version of the press release is here. Read the full complaint here. Mortgage Giant Fannie Mae Accused of Racial Discrimination in 38 U.S. Metro Areas FOR IMMEDIATE RELEASE December 5, 2016 Contact: Caroline Peattie | (415)483-7552 | peattie@fairhousingnorcal.org SAN RAFAEL, CA — Today, Fair Housing Advocates of Northern California (formerly Fair Housing of Marin), the National Fair Housing Alliance (NFHA), and 19 other local fair housing organizations from across the United States filed a housing discrimination lawsuit against Fannie Mae in federal district court in San Francisco, California. The lawsuit alleges that Fannie Mae maintains and markets its foreclosures (also known as real estate owned or “REO” properties) in white neighborhoods consistently better than in middle- and working-class African American and Latino neighborhoods. The lawsuit is the result of a multi-year investigation. The data supporting the federal lawsuit, which includes substantial photographic evidence, shows a stark pattern of discriminatory conduct by Fannie Mae in the maintenance of its foreclosures. During the past several years, NFHA notified Fannie Mae many times of its failure to maintain and market its foreclosed homes in communities of color at the same standard at which it was maintaining and marketing the foreclosed homes it owned in similar, predominantly white neighborhoods. In spite of numerous meetings between NFHA and Fannie Mae to address these disparities in maintenance and marketing, Fannie Mae persisted in its willful neglect of its properties in African American and Latino neighborhoods. NFHA and two local fair housing organizations conducted an intial investigation in 2009 in four metropolitan areas. Much of this evidence was shared with Fannie Mae. However, Fannie Mae failed to make changes to ensure equal treatment in the maintenance and marketing of its foreclosures in neighborhoods of color, and the investigation was expanded to include an additional 18 fair housing organizations, culminating in data from 212 cities in 38 metropolitan areas (see Table 1 for a full list of metropolitan regions and fair housing organizations involved in the lawsuit). Comprised of evidence from 2011 through 2015, the lawsuit contains information from more than 2,300 foreclosures owned and maintained by Fannie Mae. NFHA and its 20 partner fair housing organizations collected evidence at each property on over 35 data points that were identified as important to protecting, securing, and marketing the homes. Investigators also took and reviewed over 49,000 photographs of these foreclosures that document the differences in treatment. According to Fannie Mae’s website, "the mission of the Fannie Mae Property Maintenance team is to ensure the quality of our REO property maintenance services, consistently producing best-in-class, market-ready properties and maintaining them until removal from our inventory.” “Fannie Mae’s mission statement contradicts the findings of the multi-city, multi-year investigation,” said Shanna L. Smith, President and CEO of NFHA. She continued, “Fannie Mae executes its mission in predominantly white neighborhoods, but certainly the evidence in the complaint and the photographs illustrates that its foreclosures in middle- and working-class neighborhoods of color are not maintained as ‘best-in-class’ and they are not even close to ‘market-ready.’” Fannie Mae-owned properties in predominantly white working- and middle-class neighborhoods are far more likely to have the lawns mowed and edged regularly, invasive weeds and vines cleared, windows and doors secured or repaired, litter and trash removed, leaves raked, and graffiti erased from the property. Conversely, Fannie Mae-owned properties in predominantly African American and Latino neighborhoods are more likely to be left neglected with debris and trash on the property, overgrown grass, and invasive plants. The windows and doors are often unsecured, left wide open, or boarded. The poor appearance of the Fannie Mae-owned properties in middle- and working-class neighborhoods of color destroys the homes’ curb appeal for prospective homebuyers and invites vandalism because the homes appear to be abandoned. Additionally, the blight created by Fannie Mae results in a decline in home value for the predominantly African American and Latino families who live nearby, deepening the racial wealth gap and inequality in America. Poorly maintained foreclosures also have serious health consequences. According to a report by Mariana Arcaya, Sc.D., M.C.P for the American Heart Association, living near a foreclosure can increase a person’s blood pressure “due in part to unhealthy stress from residents’ perception that their own properties are less valuable, their streets less attractive or safe and their neighborhoods less stable.” Arcaya told TechTimes.com that “people may not find walking past an empty house appealing and this affects the physical activities that they engage in such as running and walking around the neighborhood.” The Fannie Mae investigation uncovered hundreds of windows and doors that were left open or broken at properties in neighborhoods of color, allowing rain water to accumulate inside the home or basement. Many photographs also show the growth of mold and discoloration of the interior and exterior walls from water damage. According to the International Code Council (ICC): Aerobiologist Darryl Morris and Dr. Joseph Leija, co-founders of Midwest Aerobiology Labs (a MoldDNA laboratory), have researched how specific molds affect infants, often leading to an increased chance of childhood asthma. . . . The final outcome was that out of the mold species that were identified, 88 percent of study foreclosed homes contained dangerous levels of Aspergillus flavus, a very infectious mold that is capable of causing human disease. Eighty-seven percent of study foreclosed homes had one or more molds that have been known to cause childhood asthma . . . and 80 percent of study foreclosed homes had dangerous levels of Stachybotrys chartarum (Black Mold), which indicated that these homes had suffered severe water damage. According to PestWorld.org news, a foreclosed home that is empty and uncared-for can attract a variety of pests, including termites, spiders, ants, mosquitoes, stinging insects and rodents. An overgrown or unkempt yard, for example, can harbor many more pests than a well-groomed yard. Small holes in siding, rips in screens, broken window glass, and cracks in the foundation provide easy access inside for pests. A rodent infestation is especially likely to spread from a foreclosed home to other nearby houses. Once rodents do invade a home, they can pose serious health and property risks. Rodents contaminate food and spread diseases like Hantavirus, a viral disease that can be contracted through direct contact with, or inhalation of, aerosolized infected rodent urine, saliva, or droppings. A number of Fannie Mae’s foreclosed properties were infested with rats upon inspection, as evidenced by the rat that Fair Housing Advocates of Northern California photographed at one Richmond, CA property (pictured below).  Smith stated, “Fannie Mae continued to neglect its foreclosures in middle- and working-class communities of color, even after we provided them with photographic evidence from 2009 through 2011. The evidence shared with Fannie Mae demonstrated differing maintenance and marketing practices between similar foreclosures in white neighborhoods and those in African American and Latino neighborhoods in Washington, DC; Prince George’s County and Montgomery County, MD; and the metropolitan areas of Atlanta, Oakland, Philadelphia, Dayton, Baltimore, Dallas, and Phoenix. Fannie Mae’s intentional failure to correct its discriminatory treatment in African American and Latino neighborhoods—the same communities hardest hit by the foreclosure crisis—can only be seen as institutional racism. This systematic and intentional neglect of foreclosed homes in communities of color devalues not only the property but the very lives of the families living in these neighborhoods. Fannie Mae also creates blight that contributes to health and safety hazards for families living near Fannie Mae’s poorly-maintained homes.” What Does Intentional Discrimination Look Like?Below are photos of middle-class homes in a neighborhood of color in Richmond, California, in a census tract that is over 95% non-white. These homes are well-maintained, with manicured lawns and nice landscaping. Below are photos of middle-class homes in a neighborhood of color in Richmond, California, in a census tract that is over 95% non-white. These homes are well-maintained, with manicured lawns and nice landscaping. Imagine having to live next door to this poorly maintained Fannie Mae foreclosure. The neighbors have to put up with a house that has dead grass in the front yard, a cardboard For Sale sign propped up in a broken window, dead shrubs, invasive plants, damaged siding, holes in the structure, wood rot, pervasive mold, and peeling paint. This Fannie Mae foreclosure has absolutely no curb appeal, yet Fannie Mae is marketing this property in this horrible condition. Pictured below are Fannie Mae-owned foreclosures in Oakland, CA in African American neighborhoods where investigators documented a wildly overgrown yard and a boarded-up home that had graffiti painted on the back of the home.  In Vallejo, CA, investigators found extensive trash that Fannie Mae failed to remove after the previous residents moved out. This type of neglect attracts rats, mice, and insect infestation, creating health hazards and blight. There is no For Sale sign, and the boarded window is an eyesore and lets everyone know that this is an abandoned, neglected property. In Fairfield, CA, this Fannie Mae-owned foreclosure in a community of color has an unsecured, boarded door —allowing squatters and vandals access to the home and putting the neighbors at great risk. Despite the warning signs posted, invasive plants, overgrown and dead shrubbery, dead grass, wood rot, trash, damaged siding, and peeling paint telegraph to everyone that Fannie Mae does not care about what happens to this property or neighborhood. BAY AREA IMPACT "There is no good, non-discriminatory reason why Fannie Mae should market and maintain their foreclosed properties in communities of color differently from those in white communities," says Caroline Peattie, Executive Director of Fair Housing Advocates of Northern California. “This is one more step in the pattern that we’ve seen where lenders divest communities of color of equity – first, by denying loans to people of color, then targeting them for unaffordable loans, then foreclosing on them, and finally failing to maintain and market those homes. The foreclosure crisis disproportionately affected non-white communities, and Fannie Mae’s failure to maintain and market those foreclosed homes harms these communities further. In the Bay Area alone, we investigated over 150 Fannie Mae-owned properties, and this pattern of neglecting properties in communities of color mirrors what other fair housing groups across the country uncovered in their investigations of Fannie Mae properties.” In the Richmond and Oakland, CA metropolitan area, Fair Housing Advocates of Northern California and NFHA investigated 88 REO properties owned by Fannie Mae. Of these, 11 were located in predominantly African-American communities; 25 in predominantly Hispanic communities; 38 in predominantly non-White communities; and 14 in predominantly White communities. 18% of the REO properties in communities of color had 10 or more maintenance or marketing deficiencies documented, and an additional 4% had 15 or more maintenance or marketing deficiencies, while none of the REO properties in White communities had 10 or more maintenance or marketing deficiencies. Here are just a few of the disparities that were documented:

In the Vallejo, CA metropolitan area, Fair Housing Advocates of Northern California investigated 68 REO properties owned by Fannie Mae. Of these, one was located in a predominantly Hispanic community; 48 in predominantly non-White communities; and 19 in predominantly White communities. We documented the following:

Fair Housing Advocates of Northern California found significant racial disparities in the majority of the objective factors we measured. Here are just a few of the disparities we documented:

NATIONWIDE STATISTICS Full statistics and data for individual cities are available at www.nationalfairhousing.org. Summary of Findings:

Highlights of Significant Racial Disparities:

Contact:

Kevin Stein (415) 864-3980 Caroline Peattie: (415) 457-5025 (Ext. 106) CIT Group Accused of Redlining and Violating Fair Housing Act CALIFORNIA REINVESTMENT COALITION AND FAIR HOUSING ADVOCATES OF NORTHERN CALIFORNIA FILE FAIR HOUSING COMPLAINT, URGING IMMEDIATE HUD INVESTIGATION INTO CIT GROUP’S ONEWEST BANK San Francisco, CA, Nov. 17,, 2016---Yesterday, two nonprofit organizations formally filed a complaint requesting that the federal Department of Housing and Urban Development (HUD) investigate whether CIT Group violated and continues to violate the Fair Housing Act through its subsidiary, OneWest Bank. In 2014, CIT Group applied to acquire OneWest Bank, and after receiving regulatory approvals, the merger was completed in August, 2015. The complaint alleges that OneWest Bank has violated the Fair Housing Act (FHA) through redlining practices such as failing to locate branches in communities of color and extending very few or no mortgage loans to borrowers of color. It also alleges OneWest maintained and marketed REO homes in predominantly white neighborhoods better than in neighborhoods of color. Read the full press release here. Read the HUD complaint here. Read the supplemental narrative here. View the map of One West REO's in the Bay Area here. Pictures are available at these links Map of OneWest branches in 2015, in MSA with minority percent greater than MSA average. Map of OneWest lending in 2014 in Majority Asian American, African American, and Latino communities. Map of OneWest REOs in the Bay Area. Map of OneWest foreclosures in Los Angeles area as compared to majority minority zip codes. Note: 68% of OneWest’s foreclosures from April 2009 to April 2015 occurred in zip codes where non-white residents represented a majority of the population in the 2010 Census. Additional foreclosures maps are available here. |

|||||

.jpg){kind=link}

{kind=link}

{kind=link}

|

|

TDD: (800) 735-2922

Se habla español We welcome our site visitors with content in Spanish and Vietnamese. En Espanol TIẾNG VIỆT |

|